The National Development and Reform Commission and the Ministry of Commerce recently announced the "Foreign Investment Industry Guidance Catalogue (Revised in 2011)". The "Catalogue" will be implemented as of January 30, 2012. In the new "Catalogue", the emphasis will be shifted from the "whole vehicle manufacturing" to the "key component manufacturing and R&D." How will this policy affect China's parts industry? The previous trend of "restructuring light zero" has caused the current automotive supply system not only to have a low degree of concentration, but also to lag behind in technology. Nowadays, the control of foreign auto parts for key auto parts is as high as 70% to 80%. The competition of local auto parts companies is mainly concentrated in non-key parts and components markets. With foreign spare parts companies scrambling to set up wholly-owned enterprises in the Chinese market, have domestic auto parts companies lost opportunities to grow together with foreign parts and components?

The growth rate of local parts and components companies is obvious to all, but compared with foreign parts and components companies, the overall gap is unavoidable.

The "Foreign Investment Industry Guidance Catalogue (Revised in 2011)" (hereinafter referred to as the "New Catalogue") will be formally implemented on January 30, 2012. This new industry policy released at the end of 2011 has caused great concern in the industry, but the New Deal has a different view on the domestic auto industry landscape. However, as the new “Catalogue†will encourage the shift of emphasis from “whole vehicle manufacturing†to “manufacturing and R&D of key componentsâ€, the development ecology of the parts and components industry will be affected. In response to this, the existence of local auto parts companies has caused widespread concern in the industry. The website has jointly conducted an industry survey jointly with the “First Financial Daily†(the investigation time was from January 16 to 29, 2012, with 2,980 participants). The results show that the industry generally believes that the local auto parts industry is likely to usher in a new round of reshuffle.

Major gap between local auto parts companies and foreign-funded parts enterprises

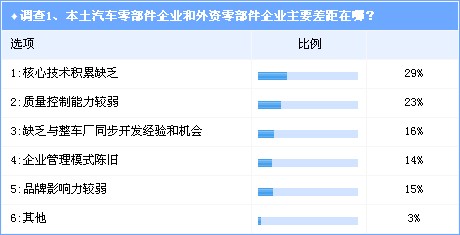

Through the poll results of Survey 1, we can see that the lack of accumulation of core technologies is still a drawback of local auto parts companies, and 29% of people in the industry believe that this is the main gap between foreign auto parts companies. The facts show that the current level of development of local parts and components companies is uneven, with the vast majority of companies only possessing the function of OEM, small scale of operation, low added value of products, weak market competitiveness, and core technologies.

Secondly, weaker quality control capability is also a serious injury to local auto parts companies. There is a clear gap between this and foreign parts and components companies, which is recognized by 23% of industry insiders. It is undeniable that at present, a large proportion of local auto parts enterprises rely on the only advantage of low labor cost, but they are constrained by the low level of quality of workers and the lack of scientific system management in the production process. The quality control of the process is not in place, resulting in a high rate of defective products and severe rework. At the same time, the theoretical understanding of the production line is not in place. There are many unreasonable phenomena in the design and staffing of the production line.

The lack of experience and opportunities for simultaneous development with OEMs, weak brand influence, and outdated corporate management are also considered by 16%, 15%, and 14% of industry insiders to be equivalent to foreign-owned parts and components companies. gap. Judging from the composition of voting proportions, local auto parts companies are not competitive enough with foreign-funded parts and components companies in all respects, and they have benefited from the rapid growth of the domestic passenger car market. As for the parts companies, with the increasing resistance of the development of autonomous car companies, the competitive situation facing them is hardly optimistic.

The formal implementation of the new "Catalogue" is likely to make the situation facing local auto parts companies more severe.

What are the implications of “manufacturing R&D for key components�

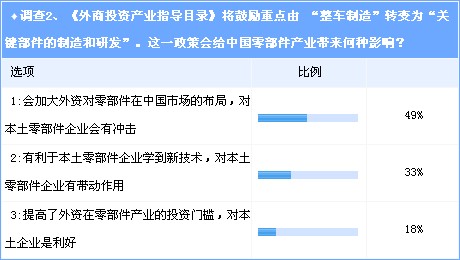

The poll results of Survey 2 show that the new “Catalogue†will encourage the shift from “whole vehicle manufacturing†to “manufacturing and R&D of key componentsâ€, which appears to 49% of industry insiders to increase foreign-invested parts and components companies. The layout of the Chinese market will have a certain impact on local parts and components companies. However, there are also 33% of optimistic people believe that this will also help local auto parts companies learn new technologies and play a positive role. Another 18% believe that this will increase the investment threshold for foreign investment in the parts and components industry, which is good for local companies.

According to the information published in the new Catalogue, with the exception of a few items such as "vehicle manufacturing" deleted from the encouragement category, the encouragement category items have generally been added, and the shareholding ratio restrictions on foreign capital in some areas have been removed. Automobile engine manufacturing and engine R&D institution construction, automobile key component manufacturing and key technology R&D, automotive electronic device manufacturing and R&D, and new energy vehicle key component manufacturing are all encouraged to invest in foreign investment.

As we all know, in the field of vehicle manufacturing, we have adopted a selective liberalization strategy for foreign investment, and set a 50:50 ratio limit, but in the auto parts area has long been completely liberalized. Thanks to its advanced technology, huge capital scale, good brand reputation and active interaction with OEMs, some foreign-funded parts and components companies have a monopoly in China. According to our understanding, the current domestic joint-venture vehicle companies The proportion of procurement from foreign companies and joint venture parts and components companies has reached approximately 90%, and some of them can even reach 100%. It is very difficult for local parts and components companies to enter the procurement system of joint-venture vehicle companies. In addition, nearly 50% of self-owned brand vehicle companies also purchase foreign parts and joint venture parts and components.

This new “Catalogue†shifts the focus of foreign investment from “whole vehicle manufacturing†to key automotive technology and components, and will undoubtedly once again drive the upgrade of the domestic parts and components industry. We believe that domestic components and parts with certain capital and research and development capabilities The company is expected to benefit from it, but it will face a test of survival for those companies that are still at the OEM level.

Therefore, to increase its own competitiveness is the key for local auto parts companies to continue inventory and development.

[next]

Faced with the continuous inflow of foreign capital, some companies with strategic vision have sought opportunities overseas to try to increase their competitiveness through overseas acquisitions.

How to look at overseas acquisitions

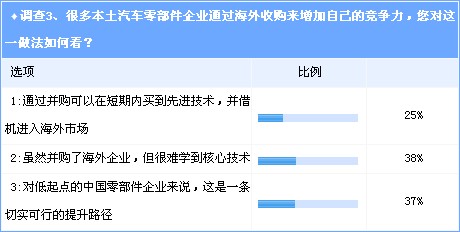

The poll results of the survey 3 showed that 38% of industry insiders believe that although local auto parts companies can acquire overseas companies, it is difficult to learn core technologies. However, the industry, which also reached 37%, believes that overseas mergers and acquisitions are a feasible way to upgrade the low-starting local auto parts companies. Another 25% believe that through overseas acquisitions, local component companies can buy advanced technology in the short term and can take the opportunity to enter overseas markets.

According to several existing large-scale spare parts overseas merger and acquisition cases (such as Beijing Pacific Century Automotive Systems Co., Ltd. acquisition of general global steering and transmission business, Jingxi Heavy Industries acquired the United States Delphi damping brake department, Wanxiang acquisition of the United States DS Based on the analysis of the above, combined with the survey results, we believe that overseas mergers and acquisitions is one of the effective ways for local auto parts companies to enhance their own competitiveness. Of course, a successful overseas merger and acquisition is based on multiple conditions, with risks and benefits coexisting. In terms of science and practice, overseas mergers and acquisitions can help improve the overall competitiveness of local parts and components companies, improve the company’s brand reputation overseas, and play a positive role in overseas business operations.

However, for most of the smaller domestic parts and components companies, they are far from achieving overseas M&A capabilities. They can only gain a share in the rising aftermarket, and they can't upgrade to the first-tier supplier system. When the status quo can be changed, the industry does not have much confidence.

When will the primary supply market improve?

Survey 4 poll results show that up to 54% of people believe that this situation is difficult to change within 10 years, 20% of the conservatives may be expected to be able to compete with foreign parts and components companies after 15 years. However, there are also 26% of optimists who hope that 5 years can change the current market structure. Our survey of many experts from Gasgoo.com’s expert advisory group revealed that, given the deepening of foreign-owned parts and components companies in the Chinese market and the breadth of the entire industry’s control, local parts and components companies should be able to share the same value. Even with the help of the government, it is difficult to make a climate without 20 years. After all, the strength of competition between the two sides is very different, and the joint-venture vehicle companies have always had the tradition of purchasing foreign-funded and joint-venture parts companies (the foreign partner of the joint-venture vehicle company has a close relationship with these parts and components companies), the monopoly pattern is difficult to break .

However, with the advancement of mergers and acquisitions by domestic vehicle companies and the new “Catalogue†that focuses on foreign investment, it will inevitably face reshuffling.

Will local parts companies face reshuffle?

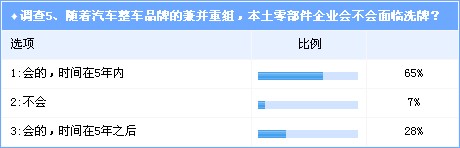

In the survey 5, as many as 65% of people think that this round of reshuffle will come in 5 years, and 28% of people expect it to be 5 years later. In contrast, only 7% of people believe that local parts companies do not exist and therefore face the industry reshuffle problem. In 2011, the growth rate of China's automobile market has slowed down significantly, and competition in the industry is bound to intensify. Some small and medium-sized local parts and components companies have already felt pressure from the outside. Once some vehicle companies are merged and reorganized, the original supplier system will be reconstructed. Many secondary and tertiary suppliers who struggle to survive at the bottom of the market will not be able to adapt to business changes and make positive adjustments. It is likely that It will also be eliminated in the fierce competition. This is the market survival rule.

How to improve the overall competitiveness of local parts companies is a major topic that involves how to develop the national auto industry. Faced with the year-by-year reduction in demand for indigenous parts and components by autonomous vehicle companies, the pressure on subsistence for local parts and components companies may be much greater than we had expected. In the end, the decision to go depends on the clear understanding of the company and its future. Development confidence. However, we also believe that the government should play not only the savior but also a leader at this time, actively promote mergers and acquisitions in the industry, and foster more truly competitive local component enterprise groups.

Wire Mesh,Steel Mesh,Wire Net,Stainless Mesh

Anping Xinghong Metal Wire Mesh Co.,Ltd , https://www.xinghongwiremesh.com